Prologue

After years of preparation and pilot studies, trained interviewers scattered across the country during the spring of 1963 to ask 2,600 targeted households questions about their household assets, debt, income, and related circumstances. Not unlike today, a small number of households held a substantial share of the nation’s wealth and were reluctant to reveal their good fortune. Piercing this veil required sophisticated oversampling along with a carefully crafted questionnaire and detailed, field procedures. The survey results offered a revealing snapshot of the spread and distribution of the nation’s wealth.

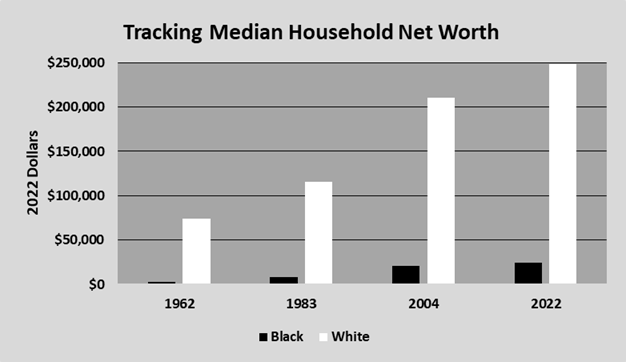

Planned and conducted while Jim Crow – the country’s system of legalized, racial segregation – remained ascendent, the published report considered how householder age, employment, and poverty status affected wealth, but no mention was given to race. Nonetheless, the survey results did offer a lucid portrait of Jim Crow America. The median White household possessed a net worth of $7,620 ($73,701 in 2022 dollars) while the typical Black household held only $295 ($2,853 in 2022 dollars). Almost one third of Black households held zero wealth or worse while less than one fifth of White households suffered the same. Strikingly, the survey showed that White households – on average – were expecting to receive an additional inheritance of $208 while Black households were anticipating $1. While dismaying, these results are unsurprising given our country’s history.

The years immediately following this effort brought substantial change to American society. The Civil Rights movement garnered long overdue fruits with the passage of the Civil Rights Act of 1964 and the Voting Rights Act of 1965. Dismantling Jim Crow was now legally required. However, the absence of immediate relief fanned the smouldering embers of rage generated by centuries-long oppression that denied African Americans respect, opportunity, and basic rights. Through the remainder of the decade, city after city erupted in violent protests and acts of overt fury.

In response, President Johnson convened a blue-ribbon panel to study the underlying causes. After a seven-month investigation, the Kerner Commission as it was known, offered a clear diagnosis of the ills:

What white Americans have never fully understood — but what the Negro can never forget — is that white society is deeply implicated in the ghetto. White institutions created it, white institutions maintain it, and white society condones it. (National Advisory Commission, 1968, p.1)

No longer could White Americans pretend they didn’t know.

At a Crossroad

These circumstances presented the country with an opportunity. The nation could augment the civil rights laws by expanding access of Black Americans to the full range of political, social, and economic opportunities. It could atone for past evils by funding wealth-building programs that targeted Black households in order to shrink disparities in educational attainment, employment, income, and wealth. Belatedly, the country could cover the unpaid promissory note on opportunity made famous by Dr. King.

Targeted help to enable American households build wealth and secure economic security was nothing new. In the past, the targeting had always favored White households. From its inception, the federal government actively supported the property rights of slaveholders over any rights of the enslaved. The Homestead Act of 1862 offered free land to “any” who could reside and develop the parcel over five years, although one initially needed to be White to be eligible. In the 20th century, Federal Housing Administration (FHA) mortgages encouraged the development of 30-year, amortizing mortgages, thereby drastically reducing the barriers to homeownership. The celebrated G.I. Bill offered returning veterans access to college or professional training as well as low-interest loans to start businesses and purchase homes. These wealth-building programs all carried overt or covert racial restrictions that funneled the overwhelming share of their benefits to Whites.

However, the recently enacted Civil Rights Act of 1964 prohibited the continuation of such methods to shower benefits on Whites. Or so one might think. The strong link between race and household wealth offered a new avenue to target assistance along racial lines.

A Novel Impulse

During this period, a tireless and persuasive official with the College Board – the U.S. non-profit organization that administers the dreaded SAT exams – worked the corridors of Washington, DC to lobby for a new wealth-building program. Lois Dickerson Rice, the daughter of Jamaican immigrants, knew from personal experience the barriers and benefits of gaining a college education. She understood that the cost of higher education was simply beyond the means of many, college-ready students. Determined to remove such obstacles, Ms. Rice persuaded Congress to enact the Basic Economic Opportunity Grants (BEOG) as part of the 1972 Education Amendment to the Higher Education Act of 1965.

These grants represented a stark departure from past, federal wealth-building programs. Their disbursement was tied to family income and not race. Further, they targeted their assistance to college-ready students from low-wealth families by offering them the largest awards. The program aspired to make a college education equally available to all, no matter their economic circumstances. Unsurprisingly, the program’s design never matched the soaring rhetoric. In its first full year, the top award was enough to cover most of the cost of a public university. The grant was purposefully designed not to cover the full costs to avoid “spoiling” wealth-poor students.

Even with this limitation, the BEOGs became wildly popular as nearly two million students used them to attend college in the inaugural years. Recognizing their appeal despite their cumbersome acronym, Congress renamed the grants after one of their own, Sen. Claiborne Pell (Rhode Island Democrat) rather than Ms. Rice. Over the past half century, Pell Grants have enabled tens of millions of qualified students from low-wealth households to attend college and complete their degree. While statistics on the racial profile of Pell Grant recipients are scarce, it is clear that a disproportionate number of beneficiaries came from African-American and other marginalized communities.

Persistent Warnings

Despite their uniqueness in targeting assistance to those with the greatest need, Pell Grants offered their help using conventional means. Like any other government expenditure or grant, the actual dollars expended are easily measured and tracked from source to recipient. This transparency makes them subject to regular Congressional oversight and normal budgetary controls. Each year, their total program costs are known and forced to compete with other pressing needs for scarce, federal dollars. Knowing where the funds are distributed permits effective program reviews to ensure financial accountability. This transparency and budgetary oversight makes the competition for federal funds quite fierce with the aim of promoting government efficiency.

While Ms. Rice was working the power corridors of Washington, Assistant Treasury Secretary Stanley was warning against the emergence of a “back door” to US Treasury that eluded these rigorous controls. Back then, Title 26 of the Internal Revenue Code – the register that lists the federal tax statutes, regulations, and interpretations – ran to thousands of pages. Buried in this legal minutiae are special exemptions given to taxpayers based on particular circumstances. For example, interest paid on a home mortgage can be deducted from one’s taxable income while interest paid on credit card debt cannot. In this way, Congress designs specific exemptions in the tax code to favour some behaviours in order to enact desired, policy outcomes.

Surrey labeled this use of tax policy as tax expenditures since they represented an alternative to using government grants and expenditures to effect change. He cautioned against their use because they lacked the transparency associated with conventional expenditures. Functioning like entitlements that ignore budgetary limits, their actual costs result from taxpayers’ choices, not budget directives. They leave no paper trail as they simply lower what taxpayers owe and thereby generate “lost revenues” for the treasury. Lacking a clear price tag, they also avoid Congressional oversight which offers them enviable obscurity.

Even when they experience the scrutiny of policymakers, Surrey warned many tax expenditures defy an accurate assessment of their impact. Many tax deductions appear neutral in design yet function as a “an upside-down subsidy” to the wealthy given the complexities of the American tax code. All of these qualities enable them to operate under the radar as stealth policies.

To discourage their misuse, Surrey proposed a full accounting of their costs in the name of government accountability and efficiency. Although he did not achieve full oversight, his arguments did bear some legislative fruit. The Congressional Budget Act of 1974 (Public Law 93-344) directed the federal government to account the lost revenues generated by these tax expenditures annually. In that year, the Joint Committee on Taxation listed 58 tax expenditures that benefited individual taxpayers to the tune of $62 billion.

Wealth as Proxy

Secretary Surrey’s hope that required budgetary accounting would discourage their use appears naïve in retrospect. Over the past half century, the number of tax expenditures has tripled while their drain on the U.S. Treasury has grown even greater. Although significant, focusing solely on these aggregate figures causes one to ignore an essential part of the story.

Back in 1974, the tax expenditures that offered the largest benefit to households all had a common characteristic – they met the needs and circumstances of the wealthy. Four deductions offered substantial tax dollars to homeowners while none targeted renters. Several others aided households with the means to save for retirement while none helped households save for rainy days. Two targeted households able to invest in appreciating assets that carry higher risk and offer greater returns. Others exempted income from state and local bonds, charitable deductions, and payments for state and local income taxes. Collectively, these tax benefits comprised the bulk ($45 billion) of the total $62 billion offered.

Targeting assistance based on household wealth offered policymakers an unseen benefit. No longer could federal assistance funnel benefits to White households simply based on race. However, the strong link established over centuries between race and household wealth offered new opportunities. Designing entitlements that required asset ownership effectively directed those benefits to “Whites Only.” Moreover, these entitlements had the appearance of being “earned” even when their opaque nature was revealed. Awarding benefits to households who attain homeownership or engage in retirement saving rewards the very behaviors our society prizes.

Tax Expenditures over the years

All the wealth-building tax deductions that were in existence in 1975 remain today. Since then, five have avoided Congressional oversight and remained unscathed despite numerous, budgetary battles. All five operate as generous entitlements that have no limits on their largesse. They demonstrate most clearly Surrey’s warnings against their stealth qualities. Among the five are the exclusions on unrealized capital gains in estates and any income from state and local bonds. As both cater to the circumstances of the wealthy, more than 90 percent of their benefits regularly redound to White households.

Four other tax expenditures attracted Congressional attention, but only to expand their benefits. Originally, only homeowners 65 years or older could take a one-time exclusion on any capital gains (with a limit of $20,000) from the sale of their home. Today, anyone can exclude up to $250,000 ($500,000 if married) and can do so every two years! The creation of the Roth Individual Retirement Account (IRA) gave the wealthy a new tax-free vehicle to save for retirement while the limits on charitable deductions have been raised. In 2017 Congress created a new tax deduction solely for qualified business owners. As White households own homes, businesses, and pension assets to a far greater extent, they regularly collect more than 80 percent of these dollars. As Whites comprise around 60 percent of the U.S. population, this represents a substantial windfall.

One tax expenditure did suffer elimination although it was quickly reversed and later expanded. The 1986 Tax Reform Act struck the capital gains exclusion from the tax code for three years. Once resurrected, it resumed its privileged status in the tax code. Later changes allowed dividend income – an important income source for the wealthy – favorable treatment as a capital gain rather than taxed as ordinary income. Once again, White households regularly collect more than 90 percent of these benefits.

Of the dozen tax expenditures, only two have experienced a reduction in their benefit limits. A half century ago, households could deduct all interest payments including mortgage interest without limit. Today, only mortgage interest payments are subject to the deduction and only to the tune of $750,000. The remaining tax expenditure, the State and Local Tax (SALT) deduction has suffered the worst at the hands of lawmakers. Over the half century, the list of exempting taxes has been pruned down to property taxes and either sales or income taxes, but not both. Further, a limit of $10,000 was placed in 2017, although it has been raised this year to $40,000. Like the other tax expenditures, White households collect a disproportionate share of these benefits as well.

As a result, the annual cost of these 12 tax expenditures to the U.S. Treasury has skyrocketed. In 1974, they totaled $45 billion while in 2022 they showered over $1.1 trillion to recipient households. Even when one adjusts for inflation, their drain on the Treasury has more than quadrupled. As context, this level of annual disbursement is slightly below the total Social Security payments, but somewhat greater than the Medicare payments, made that year.

As White households hold a disproportionate share of assets and wealth, their share of these benefits far exceed their percentage of the population. Over the period 1988-2022, it is conservatively estimated that White households collected 87 percent of these tax benefits while Black and Hispanic households collected 5 and 3 percent respectively. In 2022, White households collected over $900 billion, a figure that continues to rise. Furthermore, White households reported receiving just under $440 billion that year in family gifts and inheritances while Black and Hispanic households each received under $10 billion.

The Devolution of Pell

Over the past half century, Pell Grants have given millions of young adults the opportunity to attend college, earn a bachelor’s degree, enter a profession, and secure some measure of financial security. These grants have provided Americans from low-wealth families an alternative life trajectory and made the country more prosperous and secure. Starting at two million students, the program doubled to 4 million in fifteen years and doubled again to 8 million in 2010. Today, despite the financial fallout from the Financial Crash, 6 million students rely on Pell Grants to finance their college education. Yet, Pell has not matched its promise of providing “equal educational opportunity” to all deserving students.

At its inception, the maximum Pell Grant of $1,400 could pay as much as 80 percent of the cost of a 4-year public university and even 40 percent of a private college. While the current top award has increased to just under $7,000, it now covers only 30 percent of a public university and 13 percent of a private education. Despite evidence of the rising cost of a college education, Congress has never been willing to raise the top award to keep pace.

Unlike tax expenditures, Pell Grants have endured annual Congressional reviews. Competing with other worthy causes for scarce federal dollars, these grants never received full funding. For many years, Congress authorized a top award, but failed to appropriate enough funds to pay that award to all eligible applicants. In response to inadequate funding, the awards were scaled back proportionately to meet the actual budget. While seemingly fair, this meant those with the greatest need took the largest hit. Despite the efforts of its Congressional allies, Pell Grants never gained the coveted status of a true entitlement.

Curiously, the program’s success led to some of this systemic underfunding. Many White parents whose income made their children too affluent to be eligible wondered why they didn’t receive similar help with paying for college. Almost immediately, they lobbied Congress in 1978 to expand the eligibility requirements to include their children; doing so redistributed scarce funds away from those with the greatest need. Later changes to ignore home equity and retirement funds when considering eligibility diffused the program’s focus further.

Although significant, these decisions were overshadowed by what followed. Speaking at a Princeton University commencement, President Clinton offered a new direction in federal student aid. He proposed new tax credits that would make the “13th and 14th years of education as universal to all Americans as the first 12 are today” (Clinton, 1996, para. 38). Once enacted, these tax credits attained the entitlement status that had always eluded the Pell Grants. Moreover, they were designed to meet the needs of affluent families and inevitably shifted help away from Pell students. Currently, their cost to the U.S. Treasury exceeds the funds given in Pell Grants.

While the use of Pell Grants remains highly popular, their chronic underfunding is contributing to a growing crisis. Forced to take larger student loans to pay for college, increasing numbers of Pell students leave college with heavier debt levels. This weighs hardest on Black students as they have limited family resources on which to draw. Further, they are confronted by an unwelcoming labor market that offers lower salaries that make debt repayment impossible. Rather than a ticket to financial security, they’re experiencing their college education as a new source of debt peonage.

Charting a New Direction

These policy decisions make clear which direction the country has moved since the challenge offered by the Kerner Commission. As the graph shows, over the past sixty years – covering the entirety of the Civil Rights and post-Civil Rights era – the wealth gap between the typical White and Black households has more than tripled, even after adjustment for inflation. Using tax policies that have remained overlooked, America has doubled down on its legacy of promoting White supremacy.

The country can choose a different path, one that acknowledges its racist past and moves to eliminate the current disparities. First, the federal government can increase Pell Grant awards to restore their initial funding level and endow them with entitlement status. Broader access to college must include the opportunity to earn a bachelor’s degree without acquiring burdensome debt.

Second, the federal government should initiate a Baby Bonds proposal that is at least as generous as the one proposed by Sen. Cory Booker (New Jersey Democrat). Based on a program initiated temporarily in the United Kingdom, this program creates a trust account for every newborn in the country. Under it the federal government makes annual deposits that vary inversely with household income and invests the funds in safe, government securities. At 18, the account holder can use the funds for prescribed purposes like paying college tuition, purchasing a home, or starting a business.

As important and as impactful as these programs would be, the current wealth gap is too wide to be bridged by these proposals, alone. At this point, nothing short of a full and effective reparations program will end the racial disparities. While such a program will indeed be expensive, a funding source does exist. A careful review of the tax expenditures discussed here could lead to the elimination of some and the overhauling of others. Such a review could save nearly a trillion dollars annually. A redirection of these funds can change the fundamental direction of the country.